U.S. Federal Reserve Chairman Jerome Powell testifies during the Senate Banking Committee hearing titled “The Semiannual Monetary Policy Report to the Congress”, in Washington, U.S., March 3, 2022.

Tom Williams | Reuters

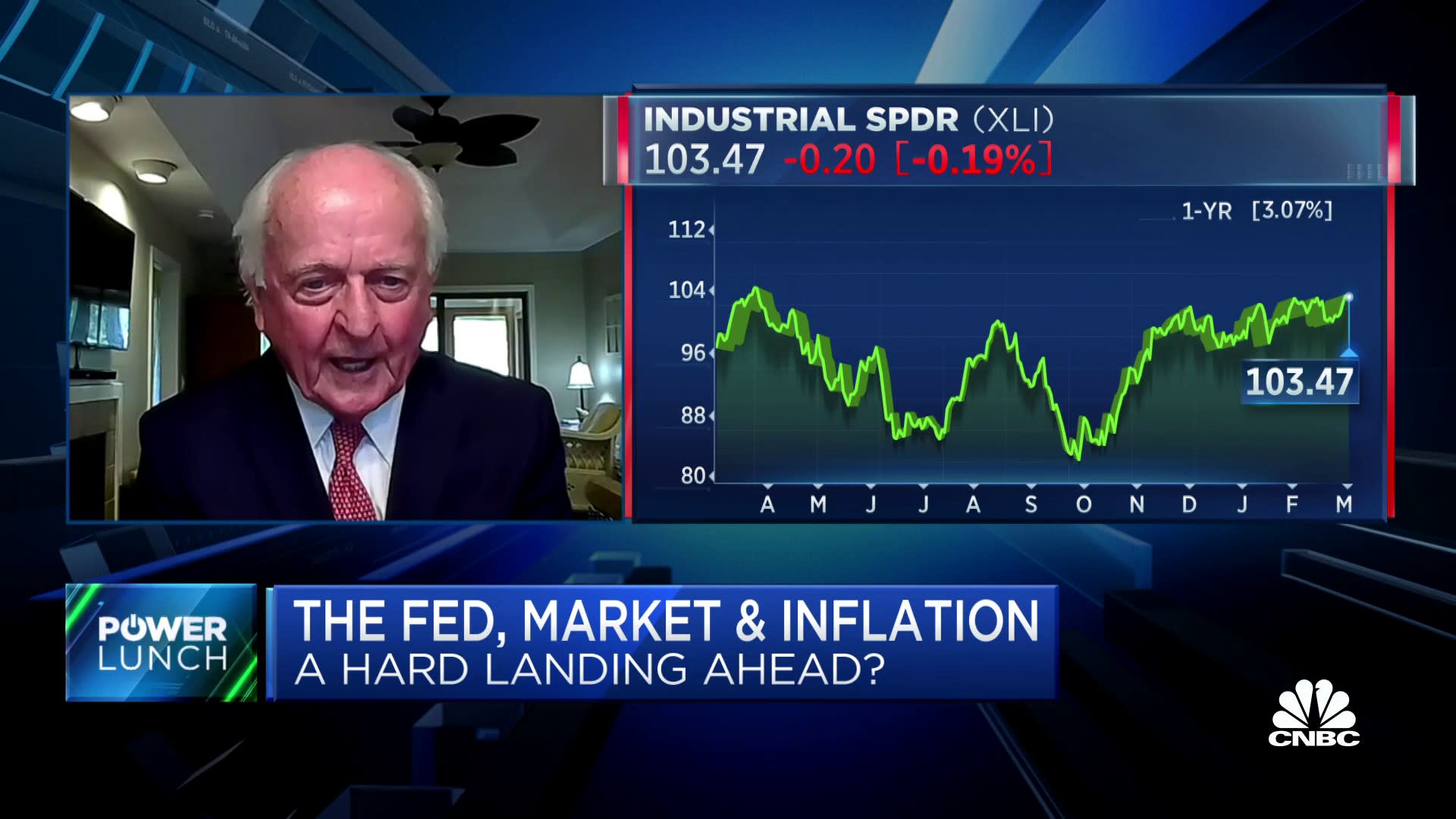

Federal Reserve Chairman Jerome Powell is set to appear before Congress with a tall task: Persuade legislators that he’s committed to bringing down inflation while not pulling down the rest of the economy at the same time.

Markets have been on tenterhooks wondering whether he can pull it off. Sentiment in recent days has been more optimistic, but that can swing the other way in a hurry should the central bank leader stumble this week during his semiannual testimony on monetary policy.

“He has to thread the needle here with two messages,” said Robert Teeter, Silvercrest Asset Management’s head of investment policy and strategy. “One of them is reiterating some of the comments he has made that there has been some progress on inflation.”

“The second thing is being really persistent in terms of the outlook for rates remaining high. He’ll probably reiterate the message that rates are staying elevated for some time until inflation is clearly solved,” Teeter said.

Should he take that stance, he’s likely to face some heat, first from the Senate Banking Committee on Tuesday, followed by the House Financial Services Committee on Wednesday.

Democratic legislators in particular have been worried that the Powell Fed risks dragging down the economy, and in particular those at the lower end of the wealth scale, with its determination to fight inflation.

Slow out of the blocks

The Fed has raised its benchmark interest rate eight times over the past year, most recently a quarter percentage point increase early last month that took the overnight borrowing rate to a target range of 4.5%-4.75%.

Markets also have been torn between wanting the Fed to bring down inflation and being worried that it will go overboard. The central bank’s slow start in tackling the rising cost of living has intensified fears that there’s virtually no way it can bring down prices without causing at least a modest recession.

“Inflation is a pernicious problem. It was made worse by the Fed not recognizing it in 2021,” said Komal Sri-Kumar, president of Sri-Kumar Global Strategies.

Sri-Kumar thinks the Fed should have attacked sooner and more aggressively — for instance, with a 1.25 percentage point hike in September 2022 when inflation as measured by the consumer price index was running at an 8.2% annual rate. Instead, the Fed in December began reducing the size of its rate hikes.

Now, he said, the Fed likely will have to take its funds rate to around 6% before inflation abates, and that will cause economic damage.

“I don’t believe in this no-landing scenario,” Sri-Kumar said, referring to a theory that the economy will see neither a “hard landing,” which would be a steep recession, nor a “soft landing,” which would be a shallower downturn.

“Yes, the economy is strong. But that doesn’t mean you’re going to glide by with no recession at all,” he said. “If you’re going to have a no-landing scenario, then you’re going to accept 5% inflation, and that’s politically unacceptable. He has to work on bringing inflation down, and because the economy is so strong it’s going to get delayed. But the more delay you have in recession, the deeper it’s going to be.”

‘Ongoing increases’ ahead

For his part, Powell will have to find a landing spot between the competing views on policy.

A monetary policy report to Congress released by the Fed on Friday that serves as an opener for Powell’s testimony repeated oft-used language that policymakers expect “ongoing increases” in rates.

The chairman likely “will strike a tone that is both determined and measured,” Krishna Guha, head of global policy and central bank strategy at Evercore ISI, said in a client note. Powell will note the “resilience of the real economy” while cautioning that the inflation data has turned higher and the road to taming it “will be lengthy and bumpy.”

However, Guha said that Powell is unlikely to tee up a rate hike of a half-point, or 50 basis points, later this month, which some investors fear. Market pricing on Monday pointed to about a 31% probability for the larger move, according to CME Group data.

“We think the Fed hikes 50bp in March only if inflation expectations, wages, and services inflation reaccelerate dangerously higher and/or incoming data is so strong the median peak rate ends up going up 50,” Guha wrote. “The Fed cannot end a meeting further from its destination than it was before the meeting started.”

Interpreting the data will be tricky, though, going forward.

Headline inflation actually could show a precipitous decline in March as year-over-year comparisons of energy prices will be distorted because of a pop in prices around this time last year. The Cleveland Fed’s tracker shows all-item inflation falling from 6.2% in February to 5.4% in March. However, core inflation, excluding food and energy, is projected to increase to 5.7% from 5.5%.

Guha said it’s likely Powell could guide the Fed’s endpoint for rate hikes — the “terminal” rate — up to a 5.25%-5.5% range, or about a quarter point higher than anticipated in December’s economic projections from policymakers.